Simulator

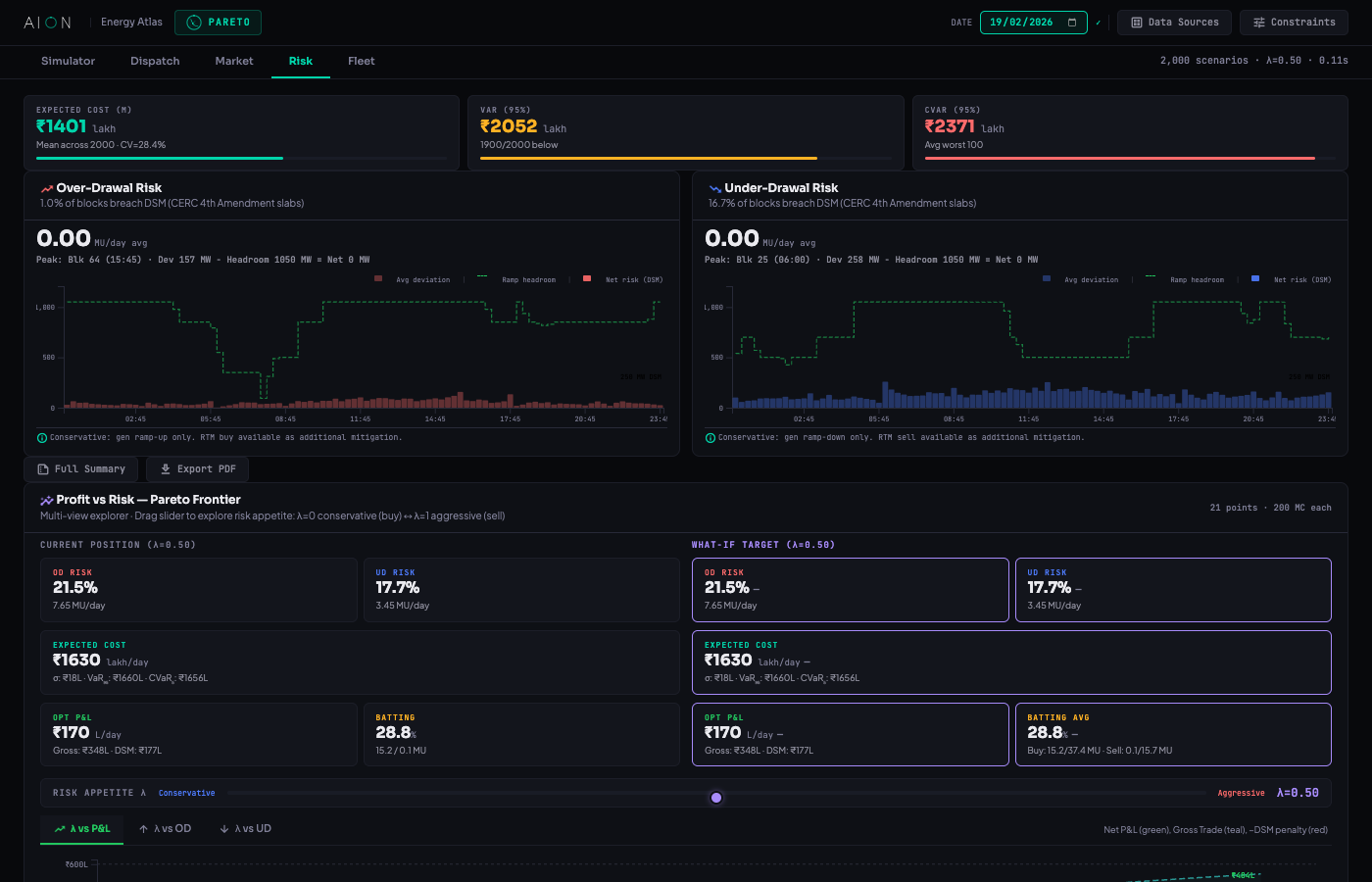

Monte Carlo CVaR-LP Optimizer

Run N stochastic scenarios with configurable risk appetite via the λ slider — from conservative (λ=0) to aggressive (λ=1). The Merit-Order + CVaR-LP engine computes optimal dispatch in under a second, producing cost distributions, VaR/CVaR metrics, and a complete cost breakdown across Gen FC, Gen VC, DAM, GDAM, Deficit Buy, Sell Revenue, and DSM Penalty.

- casino Configurable scenario count with instant RE-OPTIMIZE — results in <0.15s

- tune λ risk appetite slider — continuously adjusts cost-vs-risk tradeoff across the efficient frontier

- bar_chart Cost Distribution histogram with shaded VaR exceedance tail — visualize the full probability distribution

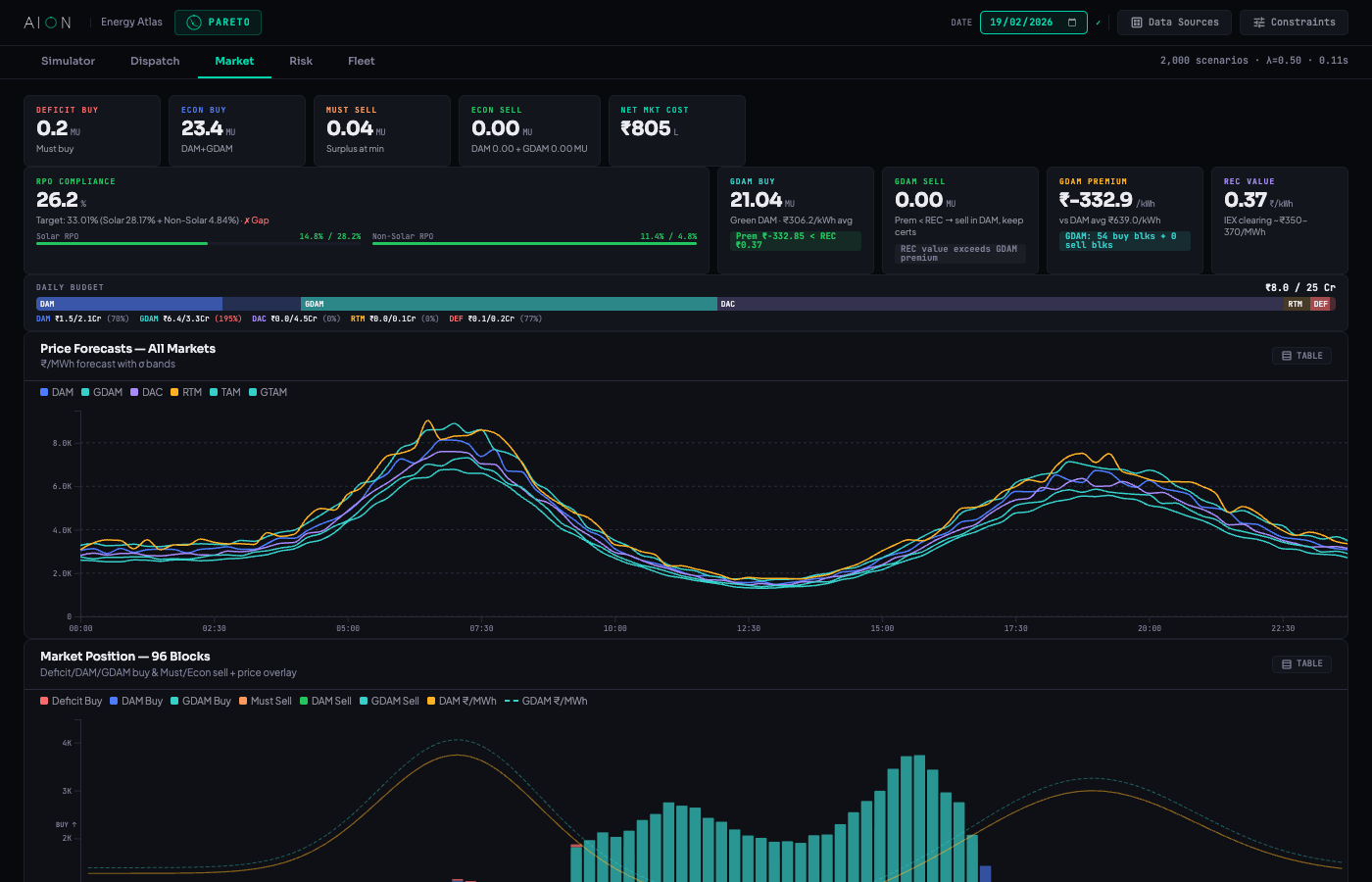

- payments Cost Breakdown: Gen FC (sunk), Gen VC (dispatch), DAM Market, GDAM Market, Deficit Buy, DAM Sell Rev, GDAM Sell Rev, DSM Penalty

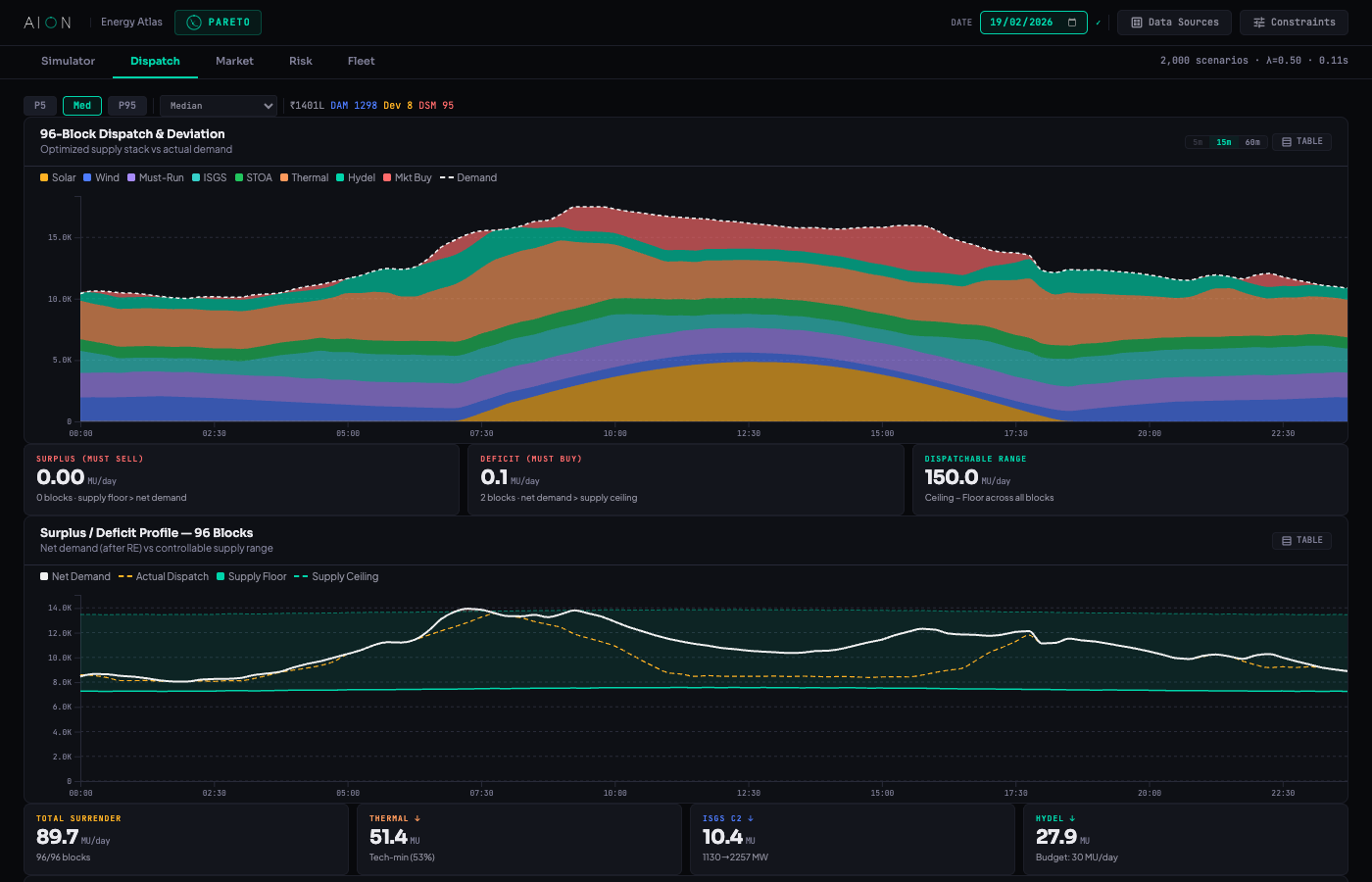

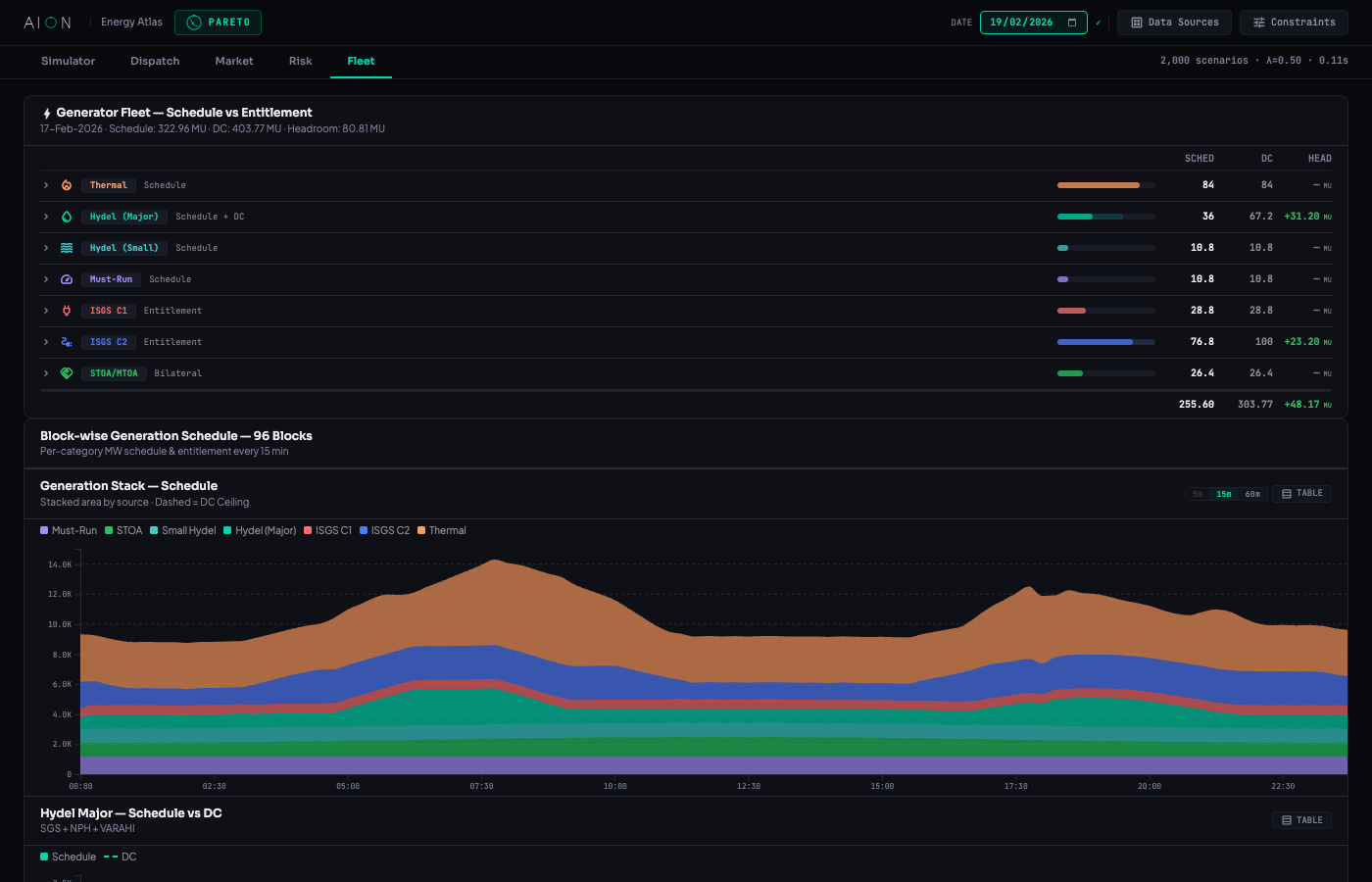

- stacked_line_chart Optimized Dispatch — stacked supply vs. demand at 5m/15m/60s resolution (Solar, Wind, Must-Run, ISGS, STOA, Thermal, Hydel, Mkt Buy)

- grid_on Block decision ribbon: Econ-buy blocks, Econ-sell blocks, Balanced blocks, Thermal backdown MU, ISGS surrender MU